Taxes and Skates

Yuriutomo personally believes that Indonesian Tax Law and Skateboarding have similarities that are difficult to separate. Both must be continuously studied and practiced because there is always a possibility that you will slip (make you dizzy) or if you are lucky then life will run smoothly until your final destination.

This website page is dedicated to research and development of tax law (based on circulars issued by the Supreme Court / Tax Court decision) that Yuriutomo learned while skateboarding and distributing drinking water to those in need. If you think this page is a solicitation or an invitation to sell and/or buy Yuriutomo products, of course, you are wrong / blundering / incorrect and it shows that you have a lot of personal problems and are not good at socializing. Moreover, it is proven that you have no friends except for orange cats (just kidding).

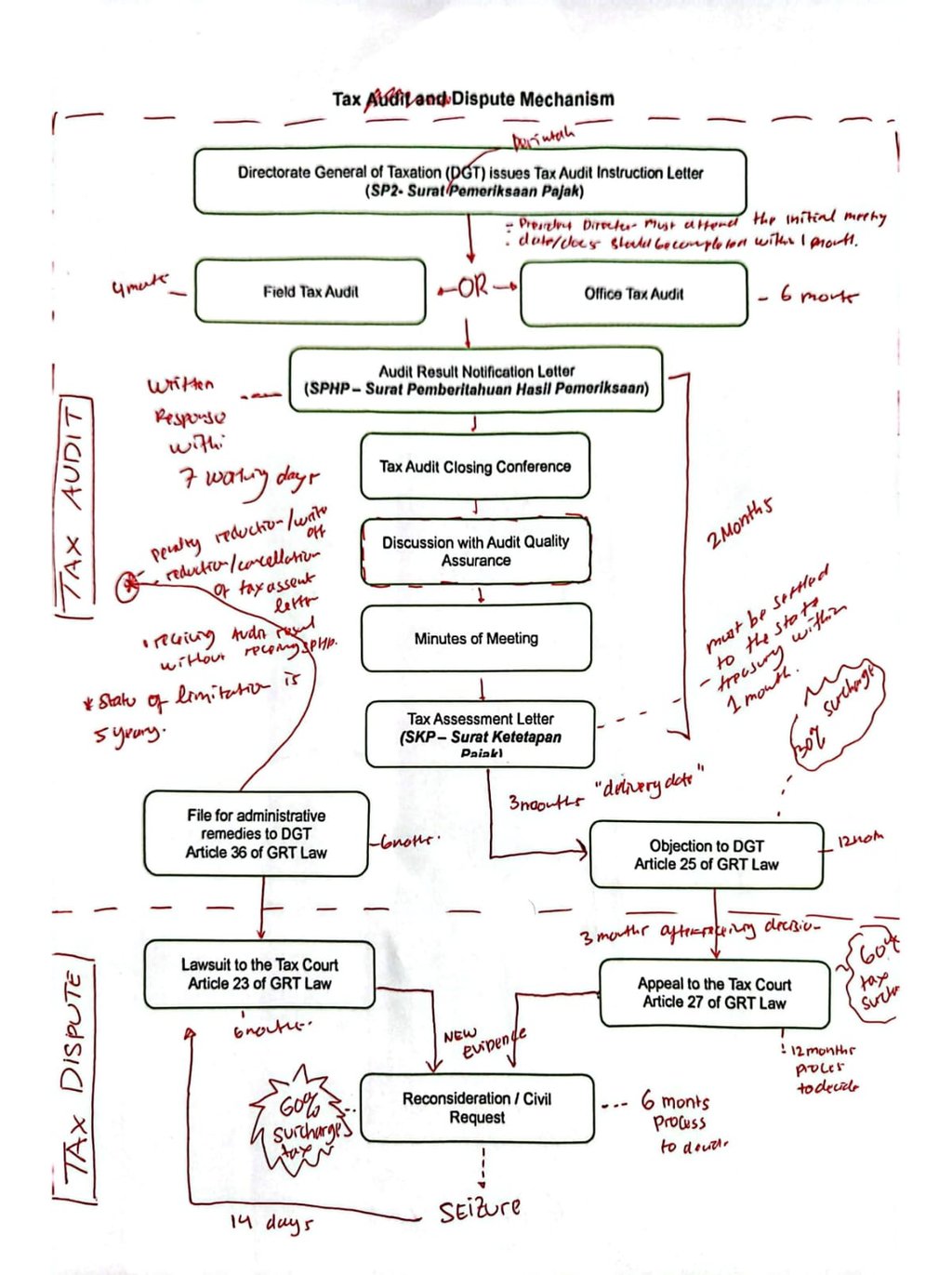

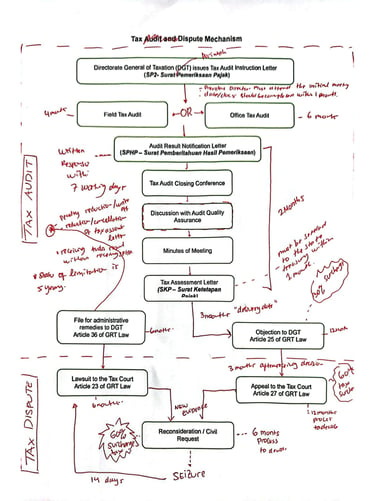

Tax Dispute Procedures in Indonesia

Tax disputes usually start with a tax audit which is then resolved in the tax court.

Supreme Court Circular Letter 2024 on Tax Disputes

Supreme Court Circular Letter No. 2 of 2024 dated 17 December 2024 regarding the Enforcement of the Results of the 2024 Supreme Court Plenary Meeting as a Guidance for the Implementation of the Court’s Tasks (“Circular Letter 2/2024”) stipulates as follows:

Palm Kernel Expeller (PKE) or Bungkil Inti Sawit

The delivery of PKE (a by-product of the crushing and expelling of all forms of palm kernel) is exempt from VAT because it is considered a certain strategic taxable good in the form of animal feed, poultry and fish and/or raw materials for the manufacture of animal feed, poultry as regulated in Article 1 paragraph (2) letter f of Government Regulation Number 81 of 2015 concerning the Import and/or delivery of certain strategic taxable goods that are exempt from VAT.

Legal remedies for taxpayers who are dissatisfied with the material/content of the determination of the amount of tax

Legal remedies for taxpayers who are dissatisfied with the material/content of the determination of the amount of tax owed are through objections and appeals based on Article 25 in conjunction with Article 27 of Law No. 28 of 2007 concerning the third amendment to Law No. 6 of 1983 on General Provisions and Tax Procedures ("Law No.6"). Examination of the authority, procedure and/or implementation of the issuance of tax decisions or determinations (implementation of writs of compulsion, writs of orders to carry out confiscation, auction announcements, preventive decisions in the context of tax collection and all matters relating to the implementation of tax decisions other than those stipulated in Article 25 paragraph 1 and Article 26 of Law No. 6) is submitted through a lawsuit based on Article 23 paragraph 2 letter c in conjunction with Article 36 paragraph 1 letter b of Law No. 6.

Exemption of VAT on 3-kilogram LPG Cylinders

In the event of a difference in the retail selling price of 3-kilogram LPG cylinders for household and micro-business purposes based on the Minister of Energy and Mineral Resources Regulation Number 28 of 2008 on the retail selling price of 3-kilogram LPG cylinders for household and micro-business purposes with the regulations/decrees of the heads of provinces, districts/cities, then the difference in the retail selling price of 3-kilogram LPG cylinders intended for public transportation services is not an object of VAT in conjunction with Article 1 of the Minister of Finance Regulation Number 80/PMK.03/2012 concerning public transportation services on land and public transportation services on water that are not subject to VAT.

Supreme Court Circular Letter 2023 on Tax Disputes

Supreme Court Circular Letter No. 3 of 2023 dated 29 December 2023 regarding the Enforcement of the Results of the 2023 Supreme Court Plenary Meeting as a Guidance for the Implementation of the Court’s Tasks (“Circular Letter 3/2023”) stipulates as follows:

Issuance of tax assessment letter after-tax crime verdict

In the event that a tax crime has been tried and decided based on a court decision that has permanent legal force, the principle of litis finiri oportet and the principle of ultimum remedium do not apply absolutely, as long as the convict still has tax obligations.

Supreme Court Circular Letter 2022 on Tax Disputes

Supreme Court Circular Letter No. 1 of 2022 dated 15 December 2022 regarding the Enforcement of the Results of the 2022 Supreme Court Plenary Meeting as a Guidance for the Implementation of the Court’s Tasks (“Circular Letter 1/2022”) stipulates as follows:

Correction of tax dispute decisions

Objections of the parties to the substance of the Supreme Court's decision considerations in tax disputes cannot be resolved by submitting an application to correct the decision error/renvoi but can only be done through the mechanism of submitting an extraordinary legal remedy.

Deemed Dividend, Tax Treaty, and Supreme Court Decision

Indonesian Supreme Court annulled all positive corrections by the Director General of Taxes (DGT) on the Income Tax Article 26 rate for service fees paid to affiliated parties.

As a background, the tax dispute is the correction of the income tax object Article 23/26 amounting to Rp.287,210,440 made by the DGT. The DGT classified it as a disguised/deemed dividend payment and imposed an Article 26 rate of 20%, resulting in a positive correction of the income tax Article 26 payable of Rp.57,442,088 which PT Rio Tinto Indonesia did not approve.

The DGT believes that based on the research he conducted, there were payments to affiliated parties for services within the business group (intra-group services) which the DGT stated could not be proven for their existence, economic benefits, and the reasonableness of the calculation of the costs paid.

PT Rio Tinto Indonesia has successfully proven that the final income tax deduction under Article 26 has been made, has been deposited into the state treasury, and has been reported in the periodic tax return. In addition, PT Rio Tinto Indonesia can prove that it has submitted a domicile certificate signed by the relevant state authority, both during the examination process and the appeal process.

PT Rio Tinto Indonesia believes that it is proven that the transaction counterparts (Rio Tinto Service Inc. Rio Tinto Singapore Holdings Pte, Ltd, and Technological Resources Pty Ltd) are residents of the Republic of Indonesia Double Taxation Avoidance Agreement partners (Tax Treaty). Following the Tax Treaty, Article 26 Income Tax of 10% is not Indonesia's taxation right.

The Supreme Court granted all of PT Rio Tinto Indonesia's requests.

Chronological order of documents

Supreme Court Decision Number 5699/B/PK/Pjk/2023, between PT Rio Tinto Indonesia against the Director General of Taxes dated January 9, 2024.

Tax Court Decision dated November 16, 2022.

Decision of the Director General of Taxes dated November 22, 2019, concerning Taxpayer's Objection to the Tax Assessment Letter for Underpayment of Income Tax Article 26 for the January 2015 Tax Period.

Tax Assessment Letter for Underpayment of Income Tax Article 26 for the January 2015 Tax Period issued on October 19, 2018.

Deemed Dividend and Shareholder Loans

The DGT believes that the loan interest rate according to the principle of fairness and customary business practice should only be 4.73% so that the difference between the shareholder loan interest rate of 6.27% (loan interest rate 11% - 4.73%) is considered a disguised/deemed dividend based on Article 18 paragraph 4 of the Income Tax Law.

PT Cirebon Electric Power disagrees with the DGT and believes that the shareholder loan interest rate of 11% is still within reasonable limits.

The Supreme Court believes that the comparative rating method according to the international rating agencies S&P and Moody’s is following the provisions, the loan interest rate of 11% is still within reasonable limits because 01 = 9.63%, 02 = 12.50%, and 03 - 13.75%. In addition, the Company's capital has been fully paid up and shareholder loans are provided in stages according to existing needs.

The Supreme Court granted all requests from PT Cirebon Electric Power.

Chronological order of documents

Supreme Court Decision Number 904/B/PK/Pjk/2024, between PT Cirebon Electric Power against the Director General of Taxes dated May 6, 2024.

Tax Court Decision dated July 27, 2022.

The decision of the Director General of Taxes dated April 29, 2020, concerning the Taxpayer's Objection to the Tax Assessment Letter for Underpayment of Income Tax Article 23 for the May 2017 Tax Period.

Tax Assessment Letter for Underpayment of Income Tax Article 23 for the May 2017 Tax Period issued on April 22, 2019.

Deemed Dividends or Management Services Agreement

PT Kraft Ultrajaya Indonesia is considered to have underpaid the Final Tax for the October 2019 Tax Period issued by the Bandung Madya Dua Tax Service Office on June 8, 2021. This is due to a positive correction to the reclassification of Article 23 Income Tax Objects amounting to Rp.6,726,465,438.

According to the assumption of the Director General of Taxes, this should be an Article 26 Income Tax Object, because the agreement is only available in English and has the same ultimate shareholders.

PT Kraft Ultrajaya Indonesia has succeeded in proving that there is a transaction for payment of management services based on a tax invoice and a valid agreement. A valid contract can be made with PT Mondelez Indonesia and PT Mondelez Indonesia Trading. Both are domestic tax subjects. The Tax Court believes outsourcing a job is an absolute activity and benefits PT Kraft Ultrajaya Indonesia as an object of tax under Article 23.

chronological order of documents

Tax Court Decision No.010869.35/PP/M/VIA Year 2024 between PT Kraft Ultrajaya Indonesia and the Director General of Taxes dated December 12, 2023.

Decision of the Director General of Taxes dated July 1, 2022, concerning Taxpayer's Objection to the Tax Assessment Letter for Underpayment of Income Tax Article 26 for the October 2019 Tax Period.

Tax Assessment Letter for Underpayment of Income Tax Article 26 for the October 2019 Tax Period issued on June 8, 2021.

Swap transactions are not objects of VAT

The subject of the dispute is the object of VAT on the use of taxable services from outside the customs area that have not been reported in the form of swap transactions/hedging transactions amounting to Rp24,276,805,200.

PT Indominco Mandiri, a company engaged in the coal mining sector, has entered into swap agreements with Engie Global Market, Morgan Stanley Capital Group, and Macquarie Bank Limited.

PT Indominco Mandiri believes that the swap transaction does not have a service element. Moreover, losses on swap transactions are not objects of VAT. Swap transactions are solely intended to maintain the stability of fuel price fluctuations.

The DGT believes that swap transactions are not exempt from VAT.

Based on the evidence, the Panel of Judges agreed with PT Indominco Mandiri that the payments made were not for the benefit of taxable services from outside the customs area, but were payments related to losses on swap transactions (purchase of fuel).

Chronological sequence of documents

Tax court decision No.PUT-006941.16/2023/PP/M.XVA of 2024 between PT Indominco Mandiri and the Director General of Taxes dated October 28, 2024.

Decision of the Director General of Taxes dated May 4, 2023, concerning Taxpayer Objection to the Tax Assessment Letter for Underpayment of VAT on Goods and Services for the use of taxable services from outside the customs area for the June 2020

Tax Assessment Letter for Underpayment of VAT on Goods and Services for the use of taxable services from outside the customs area for June 2020 issued on April 13, 2022.

For more information, please kindly email to:

Indrawan@yuriutomo.com